Introduction

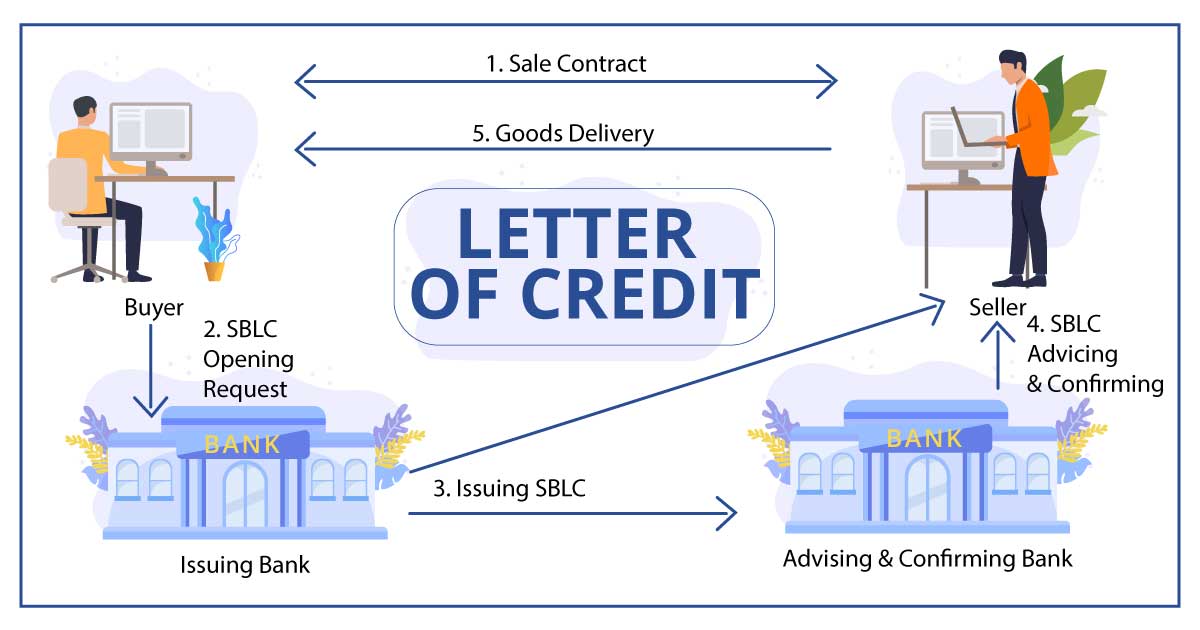

A letter of credit is essentially a bank’s undertaking to pay against the presentation of documents that comply with the terms and conditions of that undertaking. It is independent from the contract of sale on which it is based. The seller has the bank’s undertaking to pay, provided it presents compliant documents, irrespective of any dispute in the underlying contract. The confirming or issuing bank is obliged to pay if the documents presented appear to be in good order. This is known as the autonomy principle and is seen as fundamental to the successful operation of the letter of credit system.

Under English law, there are two significant exceptions to this principle:

- Illegality, where payment under the credit is prohibited by law.

- Fraud.

Fraud is an exception to the rule that a bank deals in documents alone and is obliged to pay against documents which are conformant on their face without regard to their accuracy or genuineness1. It was established on grounds of public policy, but the English courts remain cautious and require a high standard of proof, both as to the fact of the fraud and as to the bank’s knowledge, because they are reluctant to interfere with the autonomy principle.

Protection against fraud for parties in a letter of credit transaction

Buyers

Once fraud has been committed, there are very few remedies available to a buyer. Payment against documents for goods en route leaves buyers vulnerable. Prevention is therefore the best protection and due diligence on a new trading partner or unfamiliar bank will be vital.

A buyer might seek an injunction to prevent the issuing or corresponding bank paying on the basis that the beneficiary has acted fraudulently. However, such injunctions are rarely granted. In one unsuccessful case2, the Court of Appeal commented:

“If, save in the most exceptional cases, [the applicant] is to be allowed to derogate from the bank’s personal and irrevocable undertaking,.....by obtaining an injunction restraining the bank from honouring that undertaking, he will undermine what is the bank’s greatest asset,.....namely its reputation for financial and contractual probity. Furthermore, if this happens at all frequently, the value of all irrevocable letters of credit and performance bonds and guarantees will be undermined.”

Alternatively, a buyer might seek an injunction preventing the seller from relying on falsified documents. However, the court has held3 that it was not open to a buyer to seek to prevent his seller from drawing on the letter of credit, noting that the “integrity and insulation of banking contracts could be overthrown, simply by the device of injuncting the beneficiary rather than the bank”.

Seller

Fraudulent letters of credit issued or advised by fictitious banks are a risk for sellers. When dealing with a new trading partner or unfamiliar bank, sellers should seek the opinion of their own bank before proceeding.

Banks

An issuing bank can be induced to open a credit by fraudulent misrepresentation. The Court of Appeal has held4 that, unless fraud was established, any claim a bank might have against a beneficiary making a fraudulent demand must be pursued separately following payment, and cannot normally be used as a defence or set-off to avoid payment.

In one case, under UCP 5005, a confirming bank had paid under a letter of credit but it was later discovered that some of the documents presented were fraudulent. The issuing bank refused to pay the confirming bank on the grounds that the confirming bank had no greater rights than the fraudulent beneficiary. The court agreed.

In order to remedy this, article 7(c) of the UCP 600 establishes a definite undertaking by the issuing bank to reimburse the nominated bank when that bank has accepted a draft or incurred a deferred payment obligation. This has been upheld by the English court6. It is reiterated by article 12(b) of the UCP 600, which expressly provides an authority from an issuing bank to a nominated bank to discount a draft that has been accepted for deferred payment.

Corresponding banks should act with caution before refusing to pay out, even where they suspect fraud. There must be clear evidence of the fraud at the time of payment. It is insufficient merely to suspect fraud or to prove there was material which would lead a reasonable banker to infer fraud.

Where a corresponding bank is unable to seek reimbursement down the chain, one option is to bring a claim against the seller, either for restitution for mistake, or for damages for the production of deceitful documents.

The autonomy principle in letters of credit is powerful and leaves parties vulnerable to fraud, particularly in circumstances where frauds are becoming increasingly sophisticated. Prevention is the best defence available and due diligence is a key element of this, especially in relation to new trading partners or unfamiliar banks.

Whilst the UCP 600 offers consistency, it addresses fraud only to a limited extent. Parties should therefore consider which domestic law will govern should an allegation of fraud arise. Although a letter of credit is treated as one transaction, it actually involves multiple parties, multiple individual contracts, and potentially multiple jurisdictions.

-

The GLOBALG.A.P. Database

April 06 2023 -

Why food crisis will explode?

May 24 2022 -

-

-

Supply Chain 2.0:Digitizing Bananas

May 04 2022